Cryptocurrencies have transformed how we think about value, finance, and digital ownership, yet the accounting world is still catching up. Are these digital coins intangible assets like patents and trademarks, or investment instruments like stocks and bonds?

Curated by Business Science Daily — peer-reviewed sources, human-verified.

Learn more

Curated by Business Science Daily — peer-reviewed sources, human-verified.

Learn more

About Our Curation Process

Business Science Daily curates academic research in business and economics. Each featured study is selected from reputable, peer-reviewed journals, institutional repositories, or working papers (e.g., Elsevier, Sage, NBER, SSRN).

Articles are carefully summarized to ensure clarity and accuracy, with direct citations or links to original sources. Our process emphasizes transparency, academic integrity, and accessibility for a broader audience.

Learn more in our Editorial Standards & AI Policy.

The classification of cryptocurrencies within financial reporting has become one of the most contentious and conceptually rich debates in contemporary accounting. As the digital economy evolves, so too does the need for frameworks that accurately capture the economic realities of decentralized assets. In their seminal 2025 paper published in the Journal of Accounting Research, Anderson, Fang, Moon Jr., and Shipman rigorously interrogate whether cryptocurrencies should continue to be treated as intangible assets under U.S. GAAP or recognized instead as investment instruments measured at fair value.

A Research Motivation: An Asset Without a Category

Under U.S. GAAP, cryptocurrencies are currently classified as indefinite-lived intangible assets. This rule means that firms can record impairments when crypto prices fall below cost but cannot recognize gains when prices rise which is creating asymmetry in financial statements.Anderson and her co-authors question whether this approach faithfully represents firms’ economic positions. Therefore the research propositions are as follows:

H1 – Classification Hypothesis

Firms holding cryptocurrencies under the current intangible asset model (cost less impairment) report less value-relevant and less transparent information compared to fair value reporting.

- Rationale: Under U.S. GAAP before 2023, crypto assets were treated as indefinite-lived intangibles (ASC 350), meaning impairment losses were recognized, but unrealized gains were not. This asymmetry may distort firm performance metrics.

H2 – Valuation Relevance Hypothesis

Investors place less weight on reported book values of crypto assets under the cost model than they would under fair value accounting.

- Empirical focus: The authors examine market reactions and valuation multiples to assess whether reported carrying values (versus market values) affect price relevance.

H3 – Measurement Reliability vs. Volatility Hypothesis

Fair value accounting would increase earnings volatility but enhance relevance and comparability.

- Tested by: Comparing simulated fair-value-based reporting to current practice, analyzing volatility, impairment frequency, and analyst forecast dispersion.

H4 – Disclosure Quality Hypothesis

Firms that voluntarily disclose fair values or detailed crypto information have better information environments (e.g., narrower bid-ask spreads, higher analyst following).

Research Design and Methodology

The study employs a multi-method empirical approach grounded in both archival data analysis and theoretical typology development.

– Data and Sample Selection

The authors analyze a sample of publicly traded U.S. firms that reported cryptocurrency holdings between 2019 and 2023. Their data were sourced from:

- SEC filings (10-K and 10-Q reports),

- Compustat financial databases, and

- Blockchain-related disclosures tracked in firms’ notes and footnotes.

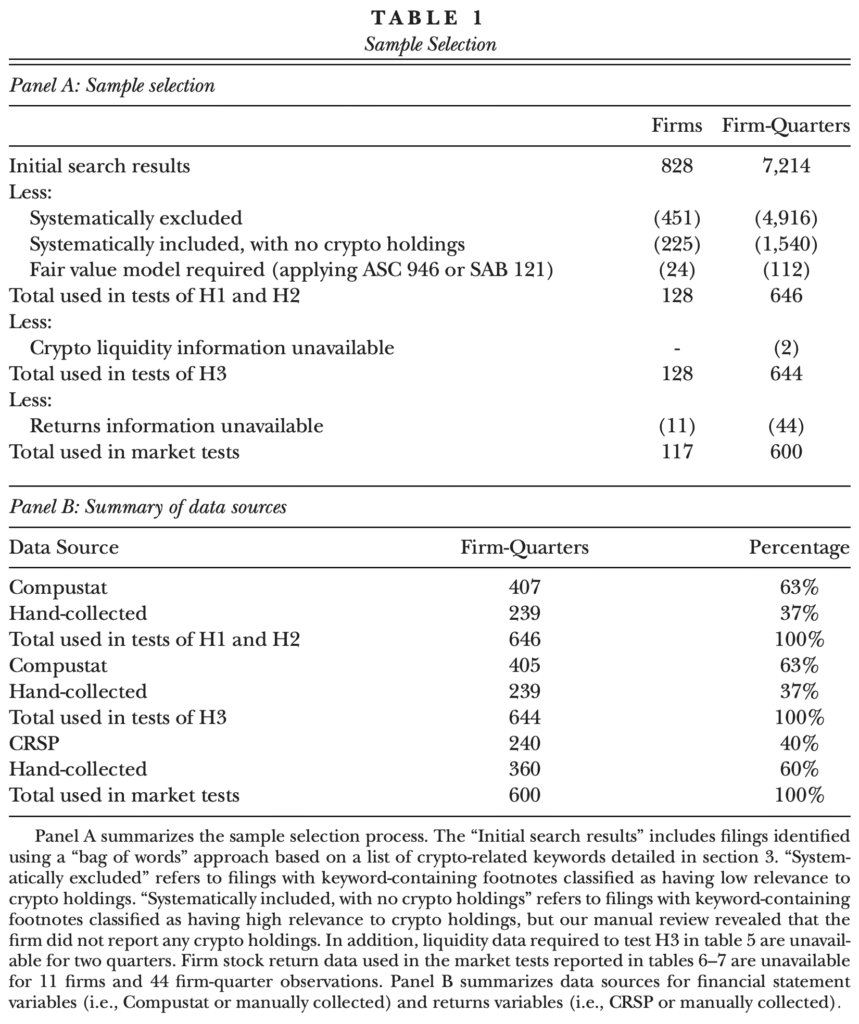

As mentioned in table 1, the final sample includes hundreds of firm-year observations, spanning technology companies, payment platforms, and diversified corporations that hold digital assets either for operational or investment purposes.

– Analytical Typology of Crypto Holdings

To classify how companies use and account for cryptocurrencies, the researchers develop a typology distinguishing between:

- Transactional holders (firms using crypto for payments or customer transactions),

- Treasury holders (firms holding crypto as part of cash management or investment strategy), and

- Strategic adopters (firms integrating crypto into business models, e.g., fintech or blockchain enterprises).

– Empirical Methods

The authors use regression analysis and valuation models to test the association between crypto holdings, reported impairments, and market valuation effects. The authors measure earnings volatility, book-to-market ratios, and stock price responsiveness to test how accounting asymmetry affects investors’ perceptions. They additionally, perform sensitivity analyses under hypothetical fair-value accounting treatments to estimate how financial statements would differ.

Reframing Crypto Through an Investment Lens

The paper makes a compelling case for reclassification. By analyzing both firm-level data and accounting theory, the authors contend that cryptocurrencies exhibit characteristics more aligned with financial investments than with traditional intangibles.

Unlike goodwill or patents, which derive value from firm-specific usage, cryptocurrencies are actively exchanged in global markets, possess observable market prices, and serve as vehicles for wealth storage and portfolio diversification. Their market-driven valuation mechanisms make them conceptually closer to equity securities than to intangible assets.

This misalignment has tangible consequences. When crypto prices increase, companies cannot record the unrealized gains, masking the true economic benefit of their holdings. Conversely, when prices fall, impairments immediately reduce reported income. The result is earnings volatility that reflects accounting asymmetry rather than genuine economic fluctuation.

Implications for Financial Reporting and Market Efficiency

By situating their argument within the broader discourse on value relevance and fair-value accounting, the authors highlight how outdated classification systems distort the informational role of financial statements.

If financial reporting is to serve investors and capital markets effectively, it must reflect assets’ economic substance, not merely their legal form. Recognizing cryptocurrencies at fair market value would enhance decision-usefulness by allowing investors to better assess firms’ exposure to risk and opportunity in volatile digital markets.

Moreover, the study’s implications extend beyond technical accounting adjustments. The authors indirectly challenge the conceptual framework of financial reporting itself by asking whether traditional asset classifications remain adequate in a digitized, decentralized economy.

The Broader Regulatory Landscape

The debate also resonates with evolving policy conversations. The Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) have both acknowledged the inadequacy of current standards. The FASB’s 2023 proposal to measure certain crypto assets at fair value represents a partial shift toward the model advocated by Anderson and colleagues.

However, regulatory progress remains incremental. The authors caution that without a coherent accounting approach, crypto-related disclosures will continue to vary widely, hampering cross-firm comparability and investor confidence.

Beyond Classification: A Theoretical Turning Point

At its core, this paper invites scholars and practitioners to reflect on how accounting theory adapts to technological innovation. Cryptocurrencies expose a long-standing tension between stewardship-based conservatism and fair-value transparency.

Anderson et al. position cryptocurrencies as a conceptual stress test for financial reporting: if accounting cannot faithfully represent assets that are digital, global, and liquid, then its underlying principles may require re-examination.

The authors thus call for a recalibration of accounting frameworks that balances prudence with informational relevance and recognizes the increasingly financialized nature of corporate balance sheets in the digital era.

Reference

Anderson, C. M., Fang, V. W., Moon, J. R., Jr., & Shipman, J. E. (2025). Accounting for cryptocurrencies. Journal of Accounting Research, 63(5). https://doi.org/10.1111/1475-679X.70018

Financial Accounting Standards Board. (2023). Accounting Standards Update 2023-08: Intangibles — Goodwill and Other — Crypto Assets (Subtopic 350-60): Accounting for and disclosure of crypto assets.https://www.fasb.org/page/Document?pdf=ASU+2023-08.pdf