By BSD –

Curated by Business Science Daily — peer-reviewed sources, human-verified.

Learn more

Curated by Business Science Daily — peer-reviewed sources, human-verified.

Learn more

About Our Curation Process

Business Science Daily curates academic research in business and economics. Each featured study is selected from reputable, peer-reviewed journals, institutional repositories, or working papers (e.g., Elsevier, Sage, NBER, SSRN).

Articles are carefully summarized to ensure clarity and accuracy, with direct citations or links to original sources. Our process emphasizes transparency, academic integrity, and accessibility for a broader audience.

Learn more in our Editorial Standards & AI Policy.

What began with targeted tariffs in 2018 escalated into a perfect storm of disruption: a protracted US-China trade war, a global pandemic that exposed systemic vulnerabilities, resurgent industrial policies, and shifting geopolitical alliances.

Many observers now see this era as standing at a turning point. At the core of this shift is a growing gap between political rhetoric and the realities companies face. A new study by Free, O’Connor, and Wieland (2026) reveals that multinational firms are charting a different, more pragmatic course. Analyzing 244 discrete sourcing shifts announced between 2018 and 2023, the researchers found that only 15.6% of relocations involved returning production to the company’s home country. Rather than staging a mass exit from China, companies are carrying out a quieter, sector-by-sector rebalancing—spreading risk across multiple countries while keeping key operations in China.

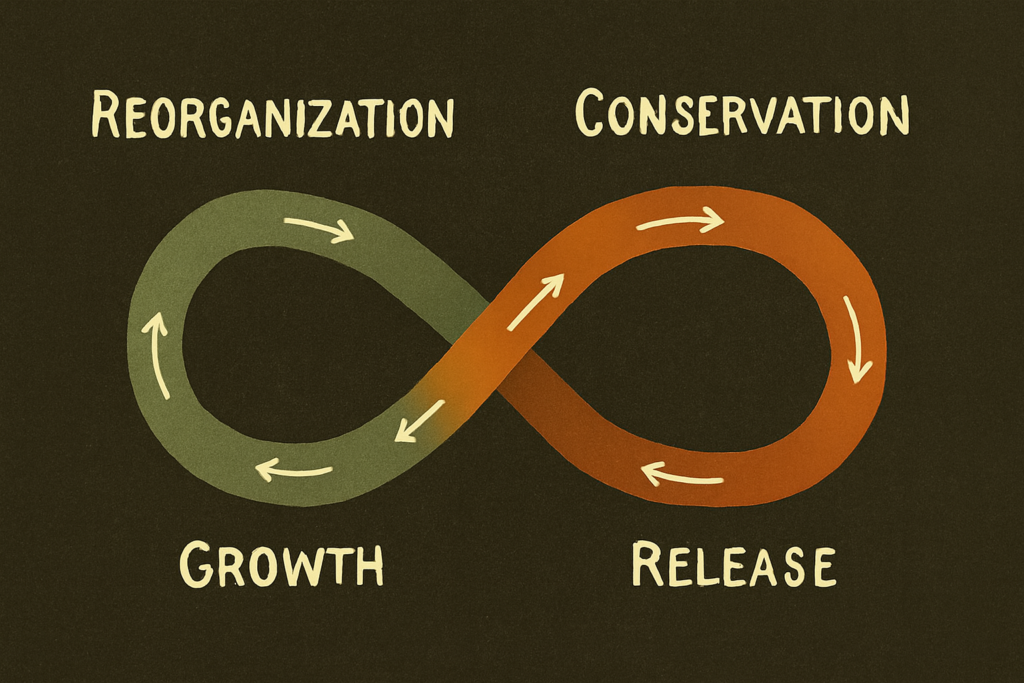

It is shown that the strategic reorganisation is not random but follows a discernible pattern of resilience-building, best understood through the lens of panarchy theory. The study also illustrates how global supply chains, as complex adaptive systems, are cycling through phases of growth, conservation, release, and renewal. The converging shocks since 2018 have triggered a system-wide “release” phase, dismantling rigid, over-optimized networks and paving the way for a “reorganisation” characterized by diversification, regionalization, and strategic ambidexterity.

To read further, navigate the interactive tabs below.

Global Supply Chains on the Move: Panarchical Reorganisation Out of China

How multinational firms are restructuring Asia-Pacific supply chains through China-plus-many diversification, revealing a significant gap between reshoring rhetoric and corporate reality.

Free, O’Connor, & Wieland (2026) investigate how Asia-Pacific supply chains reorganised from 2018 to 2023 as firms adapted to tariff escalation, geopolitical frictions, and new industrial policies. Through analysis of 244 sourcing shifts away from China, the study reveals a complex transition from conservation to reorganisation phases, with firms pursuing China-plus-many portfolios that privilege diversification over complete exit.

Summary

This study provides a comprehensive analysis of how multinational corporations restructured their Asia-Pacific supply chains from 2018 to 2023 in response to converging disruptions following the US-China trade war, COVID-19 pandemic, resurgence of industrial policy, and rising Chinese labour costs.

The Core Transformation: Global supply chains anchored in China—”the world’s factory”—entered a turbulent release phase followed by reorganisation. Firms moved from tightly optimized, China-centric networks toward diversified, multi-country sourcing configurations (China-plus-many), with Vietnam emerging as the primary beneficiary.

The Resilience Paradox: While policymakers promoted reshoring (returning production to home countries), corporate behavior told a different story. Only 15.6% of observed moves involved reshoring, with firms instead pursuing regional diversification strategies that spread risk while maintaining access to Asian manufacturing ecosystems.

Sectoral Variation: The pace and pattern of reorganisation varied significantly by industry. Labour-intensive sectors like footwear and textiles moved quickly to established regional hubs like Vietnam, while capital-intensive sectors like electronics and automotive underwent slower, phased relocations requiring substantial ecosystem development.

The study extends panarchy theory to supply chain management, showing how nested adaptive cycles unfold across industries, firms, and regions in response to macro-level geopolitical pressures.

Theoretical Framework: Panarchy Theory in Supply Chains

The study builds on panarchy theory, which conceptualizes systems as complex adaptive structures that cycle through phases of growth, conservation, release, and reorganisation across nested levels.

1. The Adaptive Cycle in Supply Chains

- Exploitation (r): Initial growth phase with loose constraints and resource accumulation

- Conservation (K): System becomes more rigid, specialized, and vulnerable to disruption

- Release (Ω): Rapid disintegration triggered by shocks, liberating stored capital

- Reorganisation (α): Resources recombine into new structures, enabling renewed cycles

2. Key State Variables

- Potential: Accumulated capital (material, energetic, social) stored during growth

- Connectedness: How tightly system components are linked (can create “rigidity traps”)

- Resilience: System’s capacity to absorb disturbance without losing core functions

3. Cross-Level Linkages

- Revolt Linkages: Lower-level disruptions (e.g., factory fire) cascade upward forcing systemic change

- Remember Linkages: Higher-level structures (e.g., institutional memory) guide local recovery

4. Resilience as Dynamic Capacity

The study reconceptualizes supply chain resilience not as a return to normalcy but as a strategic continuum involving:

- Persistence: Bouncing back to equilibrium (engineering perspective)

- Adaptability: Incremental changes to routines and resource allocation

- Transformability: Structural overhaul when existing models no longer suffice

This framework moves supply chain management from rigid control to flexible, experimental governance that encourages learning and long-term system renewal.

Methodology & Data

Research Design & Data Collection

The study employed a process-oriented methodology with temporal bracketing (2018-2023) to capture supply chain reorganisation during systemic disruption:

- Data Sources: 543 documents including media reports, company announcements, industry reports, and government statements

- Keyword Analysis: 29 keywords related to manufacturing shifts from China (e.g., “factory relocation,” “production shift,” “China decoupling”)

- Timeframe: January 2016 to March 2023, with 2018 as starting point marking trade war escalation

- Sample: 141 manufacturing firms announcing 244 discrete relocation moves

Firm Characteristics

- Geographic Diversity: Strong representation from East Asia (Taiwan, Japan, China) and United States

- Size Range: From tech giants (Apple, Microsoft) to smaller manufacturers (under $300M valuation)

- Fortune 500: 20 firms (14% of sample) including Intel, Nike, Dell, Sony, Hyundai

- Employment: Balanced between medium-sized (10,000-100,000 employees), smaller (<10,000), and large corporations (>100,000)

Analytical Approach

Coding Rationales (Gioia Method):

- 730 quoted rationales coded into 15 second-order themes

- Themes grouped into four aggregate domains: push factors from China, push factors from US, pull factors from destination countries, and internal capabilities

- Intercoder reliability: 83.5% initial agreement, 96.4% after discussion

Capacity Shift Quantification:

- Expressed in “equivalent employees” moved from China-based operations

- Calculated as: China employment baseline × percentage of capacity moved

- Data from annual reports, SEC filings, executive statements, and industry benchmarks

Key Findings

1. Geographic Patterns of Reorganisation

- Primary Destinations: Vietnam (75 moves), Taiwan (24), US (21), Mexico (20), Thailand (20), India (18)

- Regionalisation Trend: Southeast Asia emerged as critical hub, particularly Vietnam for electronics, footwear, and household goods

- Multi-Country Strategies: 66.4% of moves involved multiple destinations, with common combinations including India+Vietnam and Mexico+US

- Limited Reshoring: Only 15.6% of moves returned production to home country, despite political rhetoric

2. Sectoral Variation in Reorganisation Pace

- Labour-Intensive Industries (Footwear, Textiles): Early movers (2018-2019) to established hubs like Vietnam via “short-circuit reorganisation”

- Capital-Intensive Industries (Electronics, Automotive): Slower, phased transitions (2020-2023) requiring new ecosystem development

- Examples: Nike moved 51% of footwear production to Vietnam by 2020; Apple gradually built Indian supply chain from scratch

3. Stated Drivers of Relocation

- Primary Push Factors: Geopolitical risk (164 citations) and tariff increases (163 citations) from US-China trade war

- Secondary Factors: Rising production costs in China (54), desire to reduce China dependence (45), COVID-19 restrictions (37)

- Pull Factors: Better ecosystems (54), cheaper labour/land (43), proximity to market (51), government incentives (34)

- Multi-Factor Decisions: Firms cited average of three reasons per move, indicating intersecting risks

4. Entry Strategies and Manufacturing Models

- Existing vs. New Suppliers: 67% of moves went to existing suppliers, 33% to new partners (shifting toward new post-2021)

- Manufacturing Models: Existing moves favored contract manufacturing (48%), while new entrants preferred direct manufacturing (62.5%) for control

- Capacity Shifts: Estimated 787,072 equivalent employees moved from China, with Vietnam receiving 339,522 (43% of total)

Implications & Future Research

Theoretical Contributions

- Extends Panarchy Theory: Demonstrates applicability to socio-technical systems with concepts of “soft release” and asynchronous cycles

- Refines Resilience Understanding: Moves beyond engineering resilience to dynamic capacity encompassing persistence, adaptation, and transformation

- Integrates Agency and Structure: Shows how firm-level strategy interacts with macro-level geopolitical constraints

Practical Implications for Firms

Strategic Reorganisation:

- Adopt China-plus-many portfolios rather than binary exit decisions

- Customise pace by industry: faster moves in labour-intensive sectors, phased transitions in capital-intensive sectors

- Leverage existing supplier networks initially, then develop new partnerships as conditions stabilise

Resilience Building:

- Balance efficiency with redundancy through multi-country footprints

- Develop capabilities to track shifting policy environments and industrial incentives

- Maintain institutional memory while enabling strategic reorganisation

Policy Implications

- Move Beyond Reshoring Rhetoric: Focus on friendshoring/nearshoring and regional ecosystem development

- Build Production Ecosystems: Develop corridor agreements, cross-border logistics, and skills development across clusters (e.g., India/Vietnam)

- Reward Multi-Country Footprints: Incentivise diversification rather than single-location returns

Limitations & Future Research

- Selection Bias: Public announcements favor larger, more visible firms

- Implementation Gap: Analysed announced relocations, not necessarily implemented ones

- Capacity Estimation: Indirect methods using employment proxies introduce uncertainty

- Chinese Influence: Unable to systematically assess continued Chinese ownership/control in relocated operations

Future Research Directions:

- Extend analysis beyond 2023 to capture post-2025 tariff wave impacts

- Examine micro-processes of supplier selection, capability retention, and institutional memory

- Investigate interaction between tariff uncertainty, friendshoring incentives, and sectoral policies

- Explore design principles for modular, low-carbon supply chains in turbulent geopolitical context

References

Free, C., O’Connor, N. G., & Wieland, A. (2026). Global supply chains on the move: panarchical reorganisation out of China. International Journal of Operations & Production Management, 46(1), 46-68.

Key Theoretical Frameworks: Panarchy Theory (Gunderson & Holling), Complex Adaptive Systems, Supply Chain Resilience, Structural Ambidexterity.